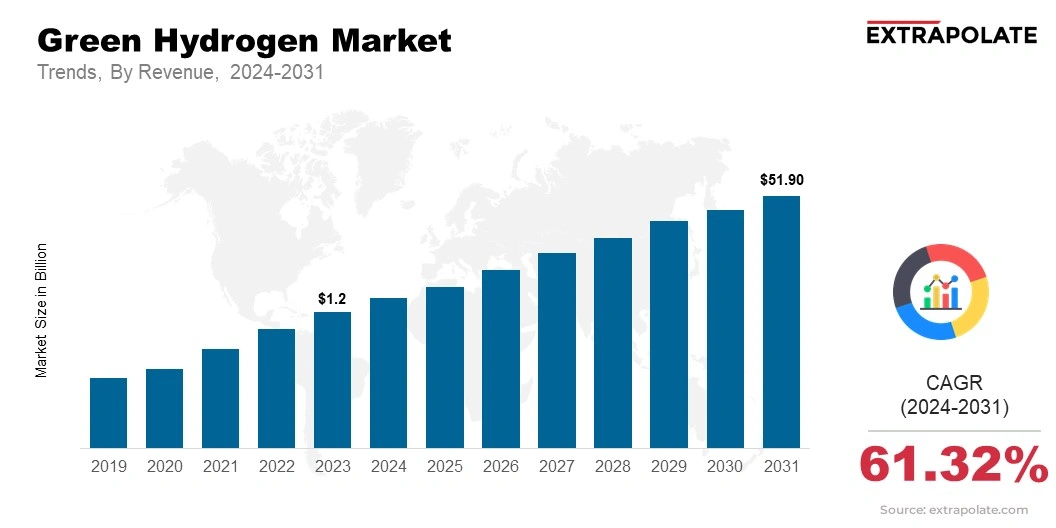

The global market is projected to reach USD 51.90 billion by 2031, growing at a CAGR of 61.32% from 2024 to 2031.

The global market was valued at USD 1.12 billion in 2023.

Increasing significance of net-zero emissions is speeding up green hydrogen adoption.

Key players in the market are Air Liquide, Linde, Siemens Energy, ITM Pwer, Nel ASA, Plug Pwer, Ballard Pwer Systems, Tshiba Energy Systems, Cummins Inc., Air Products and Chemicals, Inc.