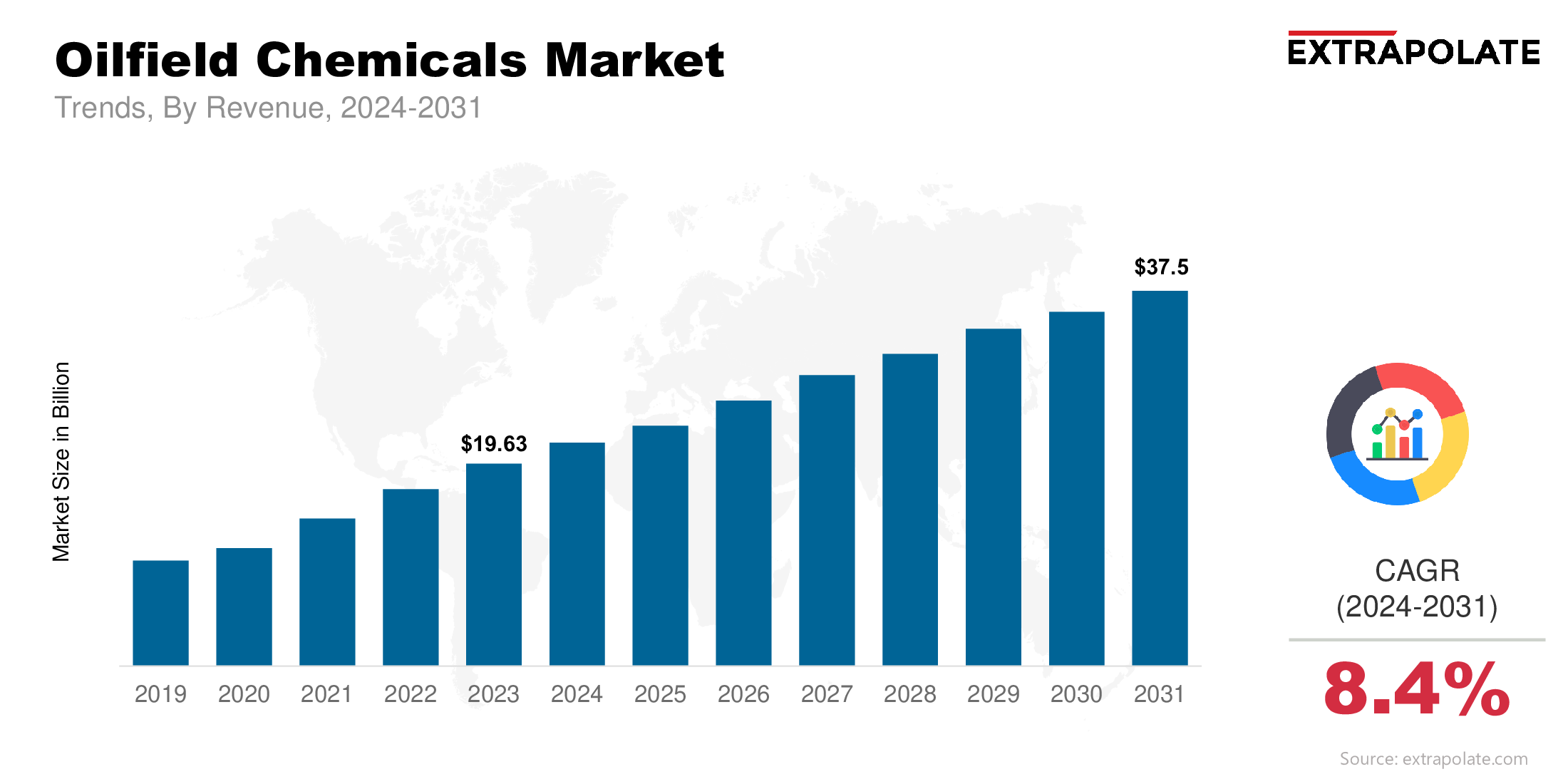

The global market is projected to reach USD 37.5 billion by 2031, growing at a CAGR of 8.4 % from 2024 to 2031.

The global market was valued at USD 21.21 billion in 2024.

The surge in unconventional energy resources, particularly shale formations in North America and deepwater reserves globally, is creating new opportunities for oilfield chemicals.

Key players in the market are Baker Hughes Company, Schlumberger Limited, Halliburton Company, BASF SE, Clariant AG, Dow Inc., Solvay S.A., Croda International Plc, Kemira Oyj, Huntsman Corporation, Ashland Global Holdings Inc., Albemarle Corporation, Stepan Company, Innospec Inc., Lubrizol Corporation and Others.