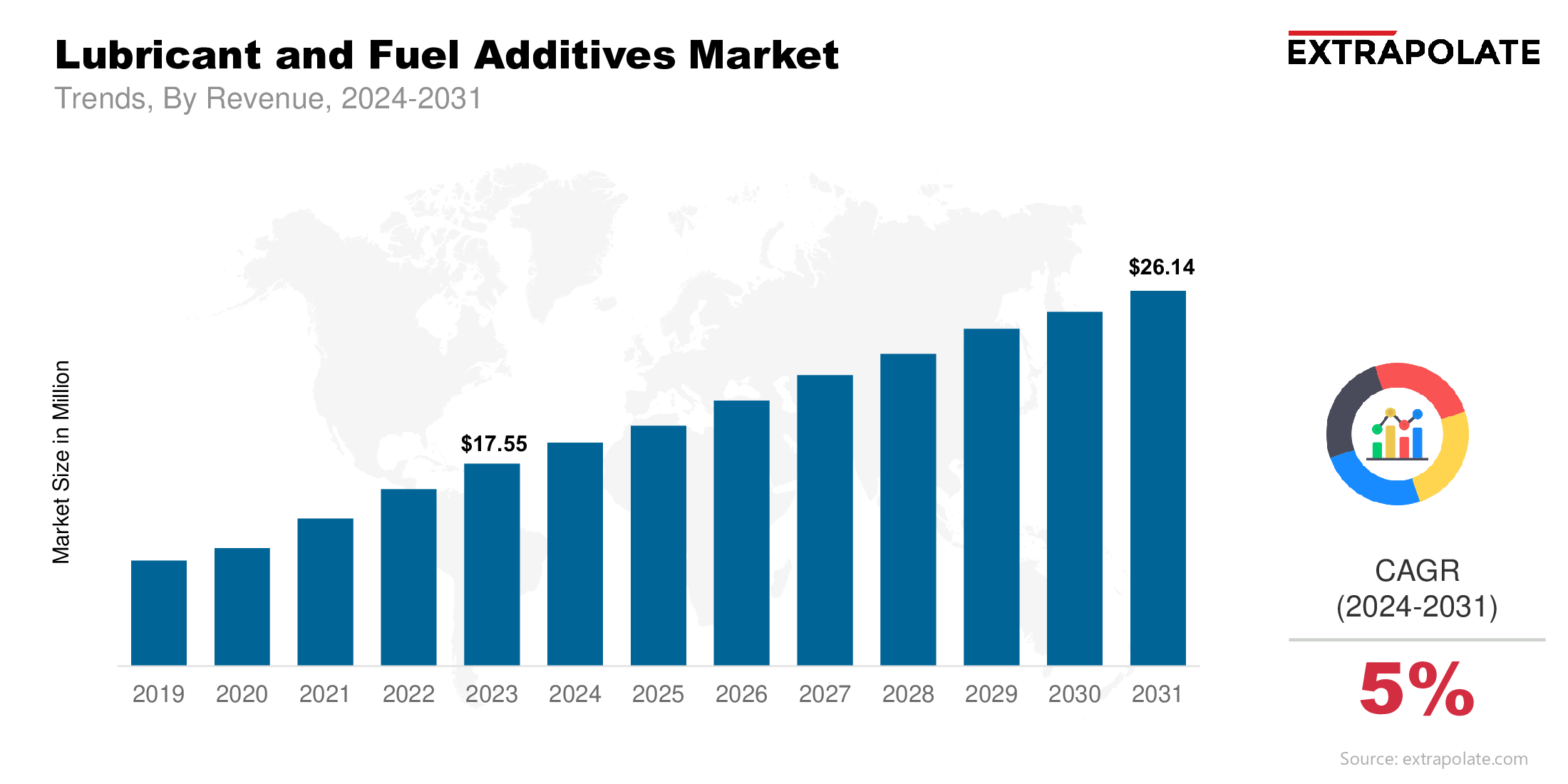

The global market is projected to reach USD 26.14 billion by 2031, growing at a CAGR of 5 % from 2024 to 2031.

The global market was valued at USD 18.48 billion in 2024.

Governments and environmental agencies are cracking down on emissions globally. Fuel and lubricant manufacturers are being forced to up the ante.

Key players in the market are Lubrizol Corporation, Afton Chemical Corporation, Chevron Oronite Company LLC, BASF SE, Infineum International Limited, Evonik Industries AG, LANXESS AG, Croda International Plc, TotalEnergies SE, Clariant AG and Others.