Key Market Trends Driving Service Adoption

Key Market Trends Driving Service Adoption

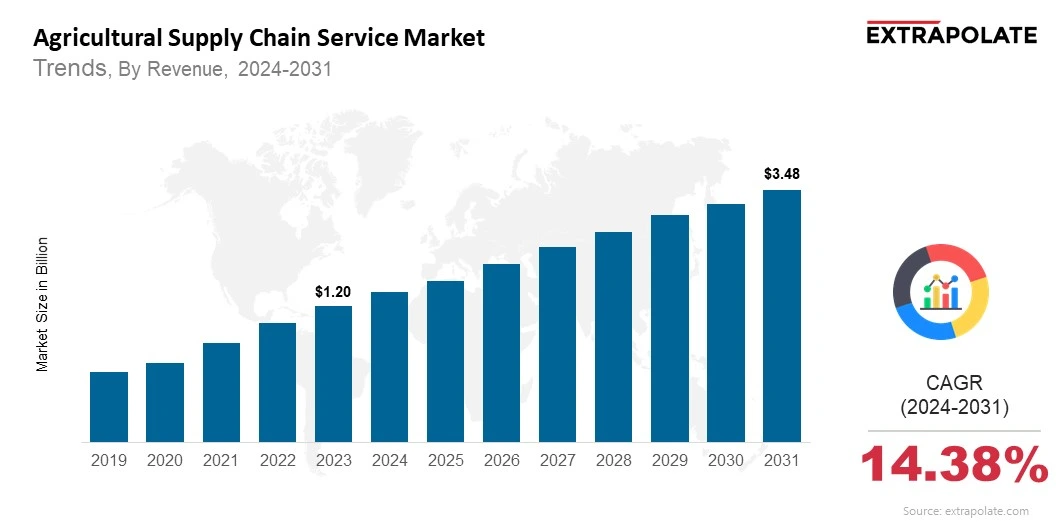

The global market is projected to reach USD 3.48 billion by 2031, growing at a CAGR of 14.38% from 2024 to 2031.

The global market was valued at USD 1.35 billion in 2024.

Key players in the market are Cargill Incorporated, Archer Daniels Midland Company (ADM), Bayer CropScience, Syngenta AG, CNH Industrial N.V., Maersk Line, DHL Supply Chain, Lineage Logistics, Olam International, CH Robinson Worldwide Inc.

Key factors that are driving the Agricultural Supply Chain Service Market growth include Investments in roads, cold chains, internet access, and storage are expanding supply chain services.