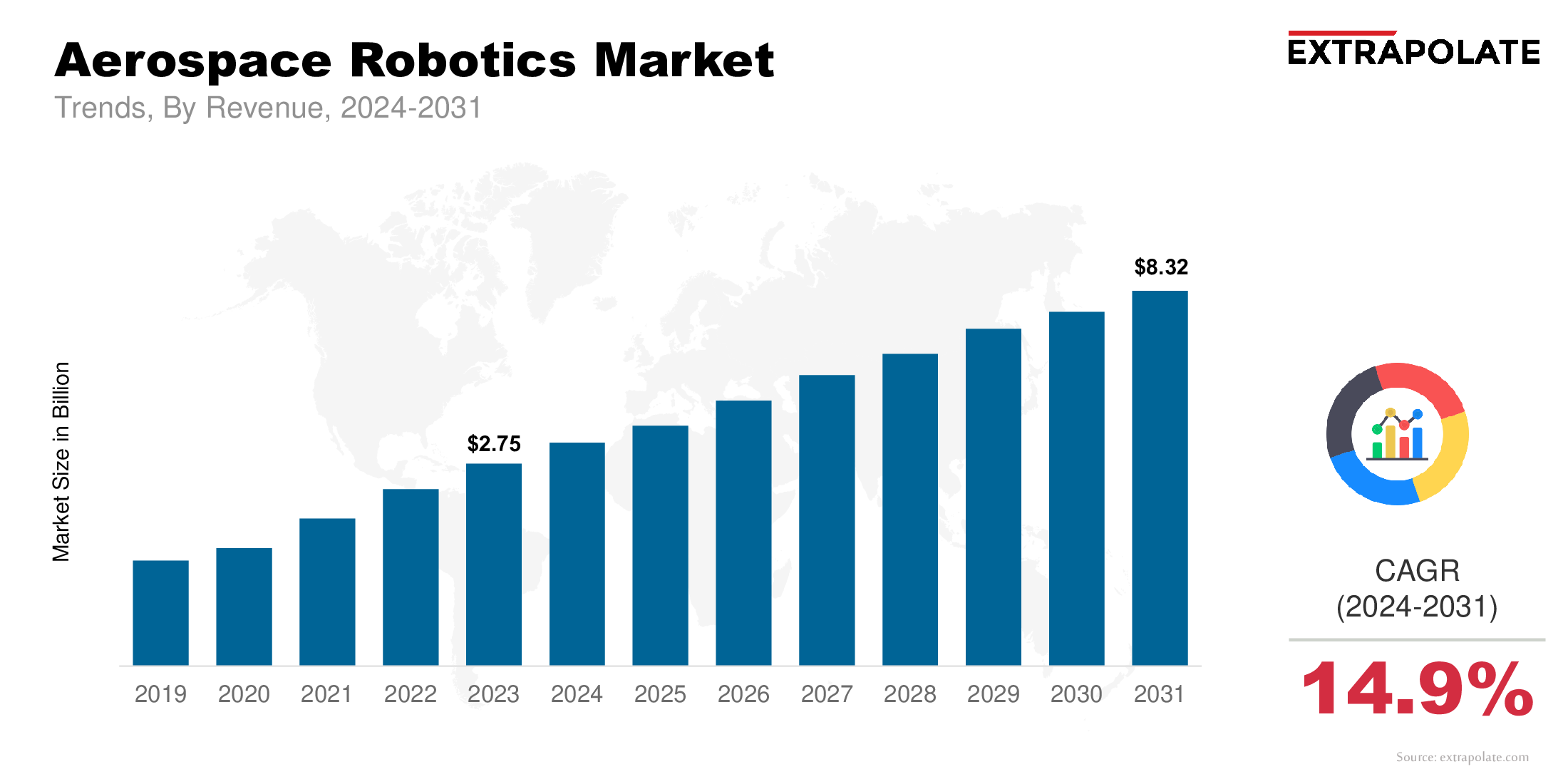

The global market is projected to reach USD 8.32 billion by 2031, growing at a CAGR of 14.9 % from 2024 to 2031.

The global market was valued at USD 3.14 billion in 2024.

The aerospace sector is increasingly integrating robotics with artificial intelligence (AI), vision systems, and machine learning algorithms.

Key players in the market are KUKA AG, FANUC Corporation, ABB Ltd., Kawasaki Heavy Industries Ltd., Yaskawa Electric Corporation, Northrop Grumman Corporation, Electroimpact Inc., Staubli International AG, Universal Robots A/S, Teradyne Inc. and Others.