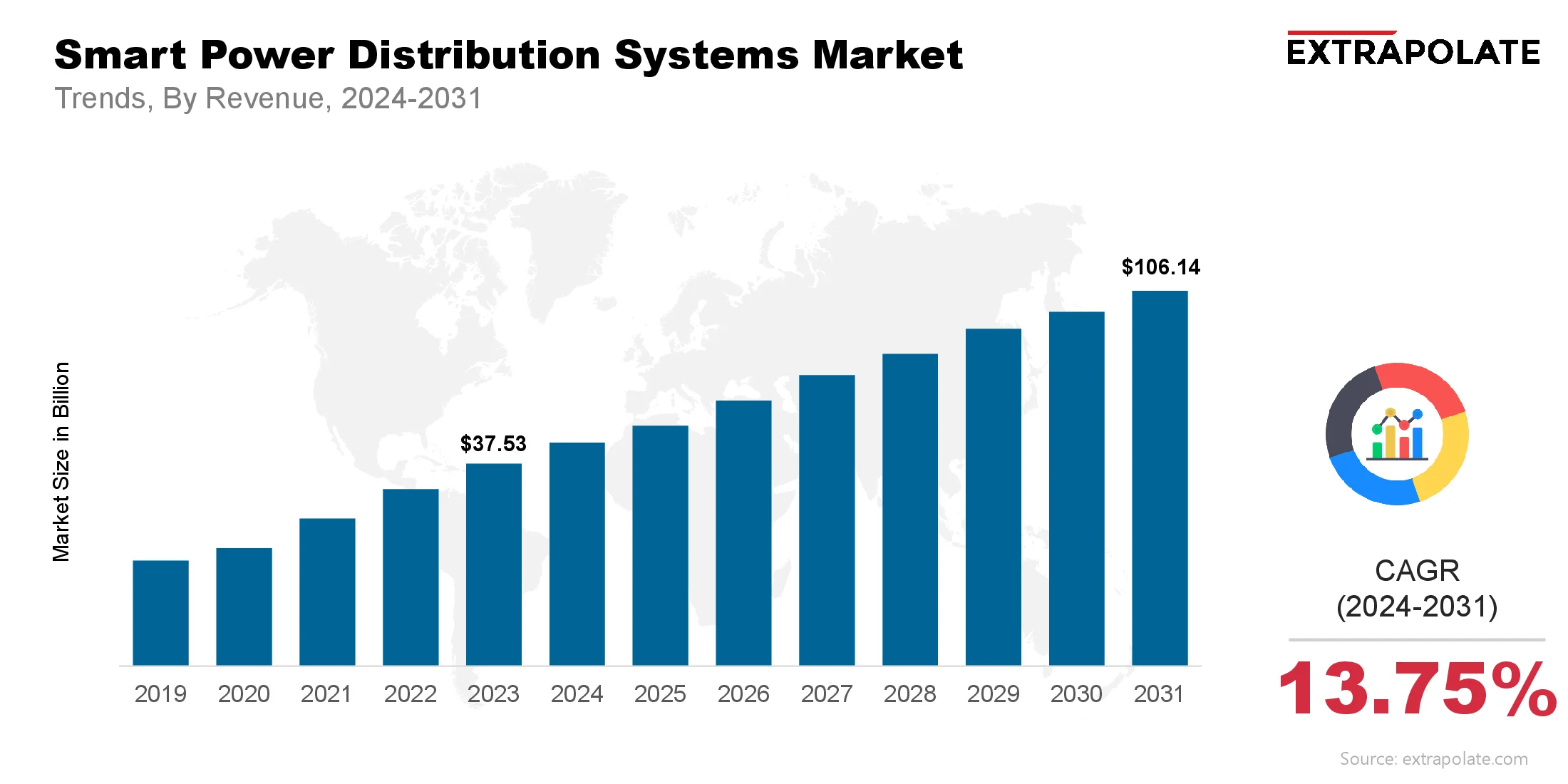

The global Smart Power Distribution Systems Market is projected to reach USD 106.14 billion by 2031, growing at a CAGR of 13.75% from 2024 to 2031.

The global Smart Power Distribution Systems Market was valued at USD 43.05 billion in 2024.

Growing cities need smarter power networks. Smart distribution Systems support smart cities by improving grid control and saving energy. Infrastructure upgrades are now key to digital plans. Governments are investing to modernize systems and boost tech growth.

Key players in the market are Siemens AG, Schneider Electric SE, General Electric Company, ABB Ltd., Eaton Corporation, Cisco Systems Inc., Honeywell International Inc., Hitachi Energy Ltd., Itron Inc., Landis+Gyr Group AG. and Others.